Economists:

Tommy Wu, PhD Lead Economist +852 3974 8839

Louis Kuijs Head of Asia Economics +852 3974 8837

Contact: Tommy Wu | tommywu@oxfordeconomics.com

- As the coronavirus outbreak and responses by governments and firms intensify globally, we have revised down our GDP growth forecast for China. We have cut our forecast for growth in Q1 by more than 2 ppts. Even with a rebound in Q2, we now forecast 5.4% growth for 2020, compared with 6% previously.

- The inopportune timing of the outbreak around Chinese New Year, a time of increased transport and economic connectivity and reduced work weeks, as well as the lockdown of affected regions all add to the equation. We expect the economic impact to mainly be felt in Q1, followed by a rebound in subsequent quarters. But a more serious and long-lasting impact cannot be ruled out.

- Travel bans will hit the tourism industry in Asia and globally, while the sharp decline in China’s Q1 growth will pose pressure on the global economy and spark fears in financial markets.

The coronavirus outbreak prompts us to revise China’s GDP growth downward

The coronavirus will hit the Chinese economy in Q1 this year. As we mentioned in an earlier Research Briefing, the economic impact is likely to be high, but short-lived, as during the 2003 SARS episode. However, the scale of the outbreak and impact is set to be worse than in the case of SARS, as the coronavirus is hitting a larger part of China and its population. Moreover, we cannot rule out an even more serious and longer-lasting impact due to differences in behaviour of the virus, a larger effect from government travel restrictions and firm closures, and a much more connected economy this time around.

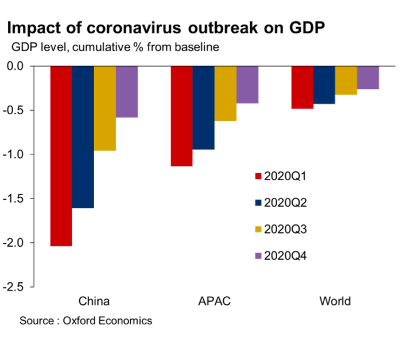

We now look for GDP to grow by 5.4% in 2020, compared with 6% forecast previously. The impact will mainly be felt in Q1, follow by an expected rebound in subsequent quarters. Our Global Economic Model suggests that the direct and indirect effects of the coronavirus on the global economy could knock around 0.25ppt off global GDP growth in 2020 as a whole, more than the 0.15ppt impact of the 2003 SARS outbreak (Figure 1).

(Figure 1)

After taking a severe hit in Q1, China, the APAC region and the global economy are expected to recover in the subsequent quarters.

We expect the impact in 2020 to equal 0.6% of GDP for China, 0.4% for APAC region as a whole and 0.25% for the global economy.

Speed of the outbreak and economic connectivity matter

Mass nationwide movement of people before and after Chinese New Year holidays present a serious challenge to the containment of the epidemic

The coronavirus outbreak has increased in severity over the past week. The World Health Organization (WHO) declared the outbreak an international public health emergency on 30 January, prompting several foreign governments to close their borders to people coming from China. While the mortality rate is lower at 2% than the 10% for SARS, the coronavirus is more contagious. It only took a month or so to reach over 17,200 confirmed cases in China and about 17,400 globally, compared to 5,327 confirmed cases in China and 8,437 globally for SARS in 2003, which lasted for seven months. The death toll was 362 by February 3, all in China except for one in the Philippines. In comparison a global total of 813 died during the SARS outbreak (of which 348 were in China).

The novel coronavirus is also more widespread across geographic regions in China than SARS. And the timing of the outbreak is a huge challenge as hundreds of millions of Chinese are on ‘travel rush’ to return home and then back to work, before and after the Chinese New Year holidays. While about 60% of confirmed cases were found in Hubei province – where Wuhan is located – there are ten other provinces that have seen at least 200 confirmed cases. In contrast, during SARS, over 80% of confirmed cases were in Beijing and Guangdong province, while three other provinces saw over 200 cases.

High transport and economic connectivity across regions mean that disruptions could result in major economic impact

Moreover, economic activity and transportation connectivity is much higher now. What’s worse, Wuhan is an important railway hub. Many trains that go through the city have been cancelled until after the third week of February. All these facts together suggest that nearterm disruption of economic activity is more widespread and could be higher this time around than during the SARS outbreak.

As during the SARS episode, we expect consumption and travel to take the hardest hit, as we discussed in the earlier Research Briefing. But we also expect that there will be significant disruption to other economic activities, though to a lesser degree than the impact on consumption.

Holiday extensions and cities lockdown cause additional impact

Holiday extensions translate into less work weeks in Q1

The extension of Chinese New Year holidays means that there are fewer effective work weeks in Q1 than usual. The central government announced the extension of the holidays by three days to end on 2 February. Following that, governments in seven provinces and two major cities (Shanghai and Chongqing) told non-essential businesses to remain closed until 9 February. The central government also agreed to extend holidays in Hubei province (where Wuhan is located) to an “appropriate extent” to help curb the virus outbreak. These regions together account for over 50% of China’s GDP, and a delay in business operation in these regions will add to the reduction in GDP growth in Q1. Meanwhile, many big companies, both domestic and global corporations, are also extending holidays or asking employees to work from home until early or mid-February.

Lockdown of affected regions affects local economies and could spill over to other regions through supply chains

The lockdown of sixteen cities in Hubei province, including Wuhan, will obviously affect economic activity in the province, and will likely spillover to other regions through supply chains. In particular, Wuhan is the home to production sites of several international carmakers including General Motors, Peugeot, Citroen, Nissan, Renault and Honda. The city also hosts bases and R&D centres of many Fortune 500 companies, particularly in the tech and health sectors. We expect the lockdown to last at least until the coronavirus outbreak is under control.

Economic impact expected to be high but short-lived

Consumption and travel would be the most impacted

While it is highly uncertain as to when the coronavirus outbreak will be contained and fade eventually, we think that it is not unreasonable to assume most of the economic impact will be felt mostly in Q1, at least for now.

We expect private consumption growth in China to experience the largest decline among the growth drivers. The lockdown of cities and public transport suspension in Hubei is clearly affecting people’s daily lives. While Hubei accounts for about 4.4% of China’s GDP, a plunge in consumption would wipe out a large portion of the province’s GDP and weigh on China’s GDP in Q1 2020. More generally, many local governments outside of Hubei have implemented epidemic prevention measures, including the suspension of cultural activities to avoid crowds gathering. Traffic bans have also been imposed on roads and highways to reduce the chance of the virus spreading across geographic regions. Citizens are staying home more than usual to avoid infection during the Chinese New Year holidays. Also, the government has stopped all domestic and outbound group and individual package tours. Retail, restaurants, transport and hospitality sectors are badly hit as a result.

Investment and production will see sizeable impact too but to a lesser degree

Fixed investment and industrial production will also be affected significantly, but less so than consumption, in our view. The reduced number of work weeks in Q1, lockdown of affected regions and likely disruption of the flows of people and goods in the near term (not just in the affected regions but more generally) will all hinder production and investment. Moreover, business sentiment will likely remain poor before the impact of the outbreak fades. However, given the transitory nature of the virus outbreak, investment and production activity will unlikely be brought to a standstill. Indeed, decisions on such activity tend to be based on the outlook beyond the very near term. Meanwhile, we think that exports will also be affected as production and logistics will likely be disrupted.

Policy easing to facilitate economic recovery down the road somewhat

That said, government action and response is providing some support to the economy. The building of emergency speciality field hospitals in Wuhan is an obvious example of how the government’s response can contribute to investment and construction. Following some recent steps, we also expect policy support targeting sectors and geographic regions that are affected. For instance, the CBIRC (bank regulator) has already urged banks to support industries that are experiencing difficulties due to the coronavirus outbreak. Some big banks also said to lower lending rates to businesses that are affected.

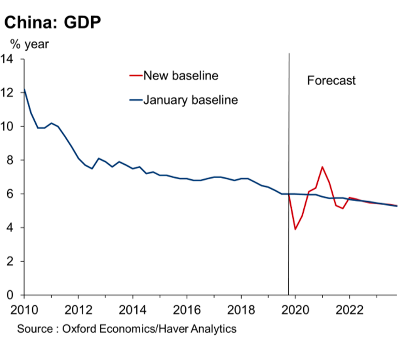

We also expect policymakers to take some measures to support the broader economy and facilitate an economic recovery, especially after the virus outbreak is under control. That said, the room for expansionary policies is smaller than in 2003. In all, we expect Q1 GDP growth to be cut by more than 2ppts – similar to the slowdown in 2003 Q2 during the SARS episode, followed by a rebound at a seasonally-adjusted annualised rate of 10% on average in Q2 and Q3. This will bring our full-year GDP growth to 5.4%, down from 6% previously (Figure 2). This translates into an impact that is equal to 0.6% of GDP in 2020. In comparison we estimated that the impact of the SARS outbreak on 2003 GDP was 0.5%.

Breaking down by GDP components, we expect a 5.7ppts impact on real private consumption in Q1, which translates into a growth of 1.1% y/y in Q1 (vs. 6.8% forecast previously). Even with a subsequent rebound, we expect consumption growth to slow to 5% in 2020 as a whole, down from an estimate of 6.8% in 2019. Similarly, we expect a 3ppts impact on real investment growth in Q1, and we look for full-year investment growth to drop to 2.9% in 2020, from an estimate of 4.2% in 2019.

(Figure2)

We expect the coronavirus outbreak to cut China’s GDP growth by more than 2ppts in Q1 – similar to the fall in 2003 Q2 during SARS, followed by a rebound in Q2 and Q3. This will bring our full-year GDP growth to 5.4%, compared with 6% forecast previously.

Travel bans will hit tourism in Asia

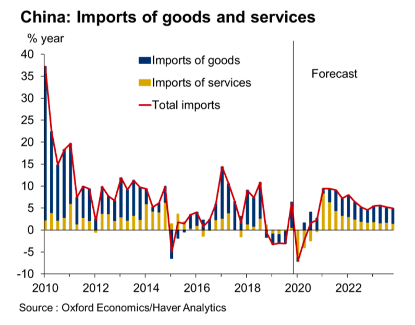

We also expect a sizeable decline in import demand in Q1, mostly due to a plunge in outbound tourism as a result of travel bans – which accounts for over 50% of imports of services in China (Figure 3). For now, we assume imports of tourism services to drop by half in Q1, though the actual outturn is subject to large uncertainty. In this regard, given that Asia-Pacific accounts for almost 80% of China’s outbound destination, economies in the APAC region that are reliant on tourism and Chinese tourists – especially Thailand – are expected to see larger downward pressure on economic growth.

When China takes a hit, so will the global economy

Meanwhile, a sharp decline in China’s growth in Q1 will pose pressure on the global economy through its import demand of goods and services other than tourism, including demand through supply chains and demand for commodities. The latter is already reflected in the recent drop in oil prices. Global financial markets have also seen a rise in risk aversion recently. Our scenario analysis suggests that the impact of the coronavirus on the wider global economy could knock around 0.25ppt off global GDP growth in 2020 as a whole.

The economic impact on China presented above represents our new baseline forecast. However, there is still lots of uncertainty as to how the coronavirus outbreak will develop both within and outside China, in terms of severity and duration. For instance, the possibility of the virus spreading significantly to the rest of Asia poses a major downside risk to the region and global growth, and would cause much larger reaction in global financial markets. We will publish estimates of the implications of more adverse outcomes in a forthcoming Research Briefing.

(Figure 3)

We expect a decline in China’s import demand in Q1, which is largely due to a plunge in outbound tourism amid travel bans.